Last Updated on May 24, 2026 by admin

Banking is one of the oldest and most important systems in human civilization. Today, people use banks almost every day for saving money, sending funds, receiving salaries, paying bills, taking loans, and carrying out business transactions. However, banking did not begin in modern buildings with computers and online applications. The history of banking started thousands of years ago when human beings first began trading goods and searching for safe ways to keep their wealth.

The origin and development of banking is closely connected with the growth of trade, commerce, agriculture, and civilization. As societies became larger and business activities increased, people needed trusted individuals and institutions to protect money, lend resources, and support economic activities. Over time, banking evolved from simple money storage into a complex global financial system that influences economies around the world.

Read: What’s the Difference between Credit Score vs Credit Rating

Early Origin of Banking

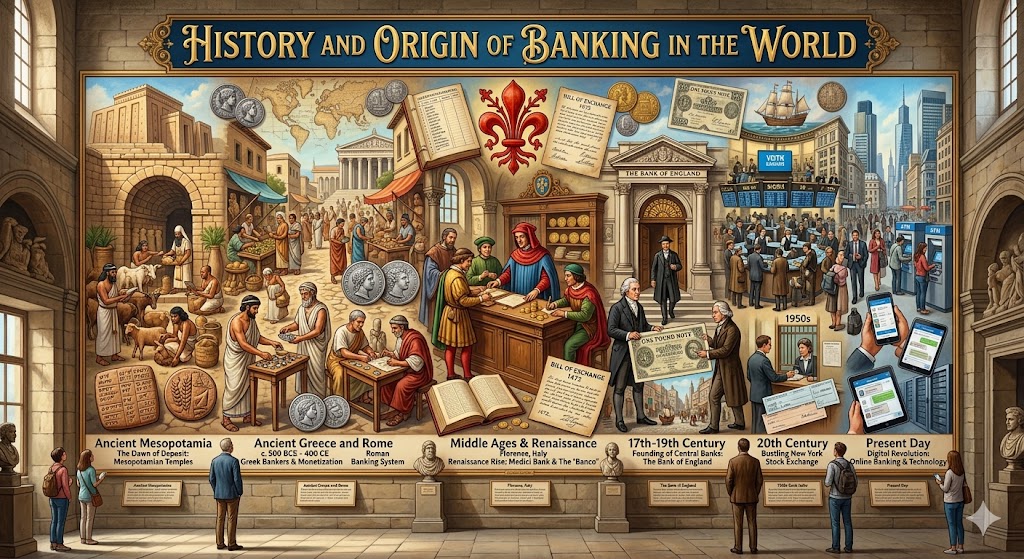

The earliest form of banking can be traced back to ancient civilizations such as Mesopotamia, Egypt, Greece, and Rome. Historians believe that banking activities began around 2000 BC in Mesopotamia, which is now part of modern-day Iraq. During this period, temples and palaces were used as safe places to store grains, gold, silver, and other valuables. Since temples were highly respected, people trusted priests and temple officials to protect their wealth.

At that time, agriculture was the main economic activity. Farmers often borrowed seeds, tools, or grains from temples and repaid them after harvest. This system became one of the earliest forms of lending. Merchants who travelled long distances for trade also deposited valuables with trusted individuals to avoid theft during their journeys.

In ancient Egypt, grain banks were common. Since grain was a major source of wealth, farmers deposited surplus grain into state warehouses. These deposits could later be withdrawn when needed. Officials kept records of deposits and withdrawals, which resembles the modern banking system.

Banking in Ancient Greece

Banking became more organized in ancient Greece around the 4th century BC. Greek temples accepted deposits from wealthy individuals and traders. Apart from temples, private bankers known as “trapezites” also emerged. These bankers operated from tables or benches in marketplaces where they exchanged coins, accepted deposits, and provided loans.

Trade played a major role in the growth of Greek banking. Since different city-states used different currencies, money changers became important. They helped traders exchange one currency for another. Greek bankers also introduced methods of transferring money without physically carrying large amounts of coins, reducing the risk of robbery.

Banking in Greece laid the foundation for several modern banking practices such as money exchange, deposits, loans, and financial record keeping.

Banking in Ancient Rome

The Romans further developed banking activities and made banking more professional. Roman bankers were called “argentarii.” They provided services similar to modern banks, including accepting deposits, lending money, financing trade, and transferring funds between accounts.

Roman law supported financial contracts and banking agreements, which helped increase public confidence in the banking system. Wealthy Romans deposited money with bankers for safekeeping, while traders borrowed money to finance business activities.

The Roman Empire had a strong road network and active trade system, which encouraged banking growth. However, after the fall of the Roman Empire in the 5th century, many banking activities declined in Europe because of political instability and economic difficulties.

Banking During the Middle Ages

After the collapse of Rome, Europe entered a period known as the Middle Ages. During this time, trade reduced significantly, and banking activities slowed down. However, banking did not completely disappear. Religious institutions and wealthy merchants continued to provide financial services.

In the medieval period, goldsmiths became important in banking history. People deposited gold and valuables with goldsmiths because they had secure vaults for storage. In return, goldsmiths issued receipts to depositors. Over time, these receipts began to circulate as a form of money because people trusted them.

Goldsmiths later realized that not all depositors withdrew their gold at the same time. As a result, they started lending part of the deposited gold to borrowers while charging interest. This practice became the foundation of modern commercial banking.

The Middle Ages also saw the rise of merchant banking, especially in Italian cities such as Venice, Florence, and Genoa. Italian merchants played a major role in international trade and needed reliable financial systems to support their business activities.

The Rise of Modern Banking in Italy

Modern banking is often linked to the Italian Renaissance period between the 13th and 15th centuries. During this time, Italy became a center of trade and commerce in Europe. Wealthy families established banks to finance trade, governments, and businesses.

One of the most famous banking families was the Medici family of Florence. The Medici Bank became one of the most powerful financial institutions in Europe. It introduced advanced banking methods such as bookkeeping, letters of credit, and branch banking.

Letters of credit allowed merchants to travel without carrying large amounts of cash. Instead, they carried documents that could be exchanged for money in another city. This reduced the danger of theft and encouraged international trade.

Italian bankers also developed double-entry bookkeeping, a system that records both debit and credit transactions. This accounting method improved financial accuracy and is still used today.

The Development of Central Banking

As trade expanded across Europe, governments recognized the need for stronger financial systems. This led to the establishment of central banks. One of the earliest central banks was the Bank of Amsterdam, founded in 1609. It helped stabilize trade and currency exchange in Europe.

Another major milestone was the creation of the Bank of England in 1694. It was established to help the British government manage debt and finance wars. Over time, it became responsible for issuing currency, controlling monetary policy, and supervising financial systems.

Central banks gradually became important institutions in many countries. They regulate money supply, maintain economic stability, and act as lenders to commercial banks during financial crises.

Banking During the Industrial Revolution

The Industrial Revolution in the 18th and 19th centuries transformed banking worldwide. Factories, railways, and large businesses required huge amounts of capital for expansion. Banks became major providers of loans and investment funds.

Commercial banks grew rapidly during this period. They accepted deposits from the public and used the funds to finance industries and businesses. Banking services became more accessible to ordinary people, not just wealthy merchants and rulers.

Countries such as Britain, France, Germany, and the United States experienced rapid banking development. Financial institutions expanded their branches and introduced new banking products to support economic growth.

The Industrial Revolution also encouraged the rise of investment banking. Investment banks helped companies raise capital through the sale of shares and bonds. This contributed to the growth of modern capitalism.

Banking in the United States

Banking in the United States developed differently from Europe. Early American banking began in the late 18th century after independence. The Bank of North America, established in 1781, became one of the first banks in the country.

In 1791, the First Bank of the United States was created to stabilize the economy and manage government finances. However, debates over federal control of banking led to political conflicts.

During the 19th century, thousands of state banks emerged across the United States. Banking regulations varied from state to state, leading to financial instability and occasional bank failures.

The establishment of the Federal Reserve System in 1913 marked a major turning point. The Federal Reserve became the central bank of the United States and helped regulate the banking industry, control inflation, and maintain financial stability.

Evolution of Banking Technology

Technology has played a huge role in transforming banking services. In earlier centuries, banking transactions were recorded manually in ledgers. Customers had to visit bank branches physically to carry out transactions.

The introduction of typewriters, calculators, and computers improved banking efficiency. By the mid-20th century, banks started using electronic systems for record keeping and customer transactions.

The invention of Automated Teller Machines (ATMs) in the 1960s changed banking forever. Customers could withdraw money and access services without entering a bank hall. Credit cards and debit cards also became widely used.

In the 1990s and early 2000s, internet banking emerged. Customers could transfer money, check balances, and pay bills online. Mobile banking later made financial services even more convenient through smartphones and applications.

Today, digital banking allows people to complete transactions within seconds from anywhere in the world. Financial technology companies, often called fintech companies, continue to introduce innovations such as mobile wallets, cryptocurrency, and online lending platforms.

Read: Definition of Credit Unions and How They Compare to Banks

Islamic Banking

Another important aspect of banking history is the development of Islamic banking. Islamic banking operates according to Islamic laws and principles, especially the prohibition of interest, known as “riba.”

Islamic banking practices can be traced back to early Islamic civilization, where traders used profit-sharing arrangements instead of interest-based loans. Modern Islamic banking began gaining global recognition in the 20th century.

Today, Islamic banks operate in many countries across the Middle East, Asia, Africa, and Europe. They provide financial services that comply with religious principles while supporting economic development.

Banking in Africa

Banking in Africa developed mainly during the colonial period. European banks established branches in African countries to support trade and colonial administration. These banks mainly served foreign businesses and government activities.

After independence, many African countries created indigenous banks to support local economic growth. Governments established central banks to regulate financial systems and issue national currencies.

In recent years, Africa has witnessed significant growth in mobile banking and digital finance. Countries like Kenya became global examples of mobile money innovation through services such as M-Pesa.

In Nigeria, banking has evolved rapidly with the introduction of online banking, mobile transfers, and cashless policies. Banks now play major roles in supporting businesses, entrepreneurship, and economic development.

Functions of Modern Banks

Modern banks perform many important functions in society. One major function is accepting deposits from individuals and organizations. Banks keep money safe and provide customers with easy access to their funds.

Banks also provide loans to businesses, students, homeowners, and governments. These loans support investment, education, trade, and infrastructure development.

Another important function is facilitating payments and money transfers. Through banking systems, people can send and receive money locally and internationally.

Banks also help create money in the economy through lending activities. They support economic growth by financing industries, agriculture, transportation, and technology.

In addition, banks provide investment opportunities, foreign exchange services, financial advice, and insurance-related products.

Challenges Faced by the Banking Industry

Despite its importance, the banking industry faces several challenges. Financial crises remain one of the biggest threats. Poor management, risky lending, and economic instability can lead to bank failures.

Below are some of the major challenges faced by the banking industry today.

Cybersecurity Threats and Fraud

One of the biggest challenges facing banks in the modern world is cybersecurity. As banking services increasingly move online, cybercriminals continue to develop sophisticated methods to steal money and sensitive customer information. Hackers target banking systems through phishing attacks, malware, identity theft, and unauthorized access to customer accounts.

Online fraud has become a serious concern for both banks and customers. Criminals often use fake websites, fraudulent messages, and phone scams to deceive customers into revealing confidential banking details. Cyberattacks can lead to financial losses, damage to reputation, and reduced customer confidence in banking institutions.

To address this challenge, banks invest heavily in cybersecurity systems, data protection, and fraud detection technologies. However, cyber threats continue to evolve, making it difficult for banks to stay completely secure.

Rapid Technological Changes

Technology has transformed the banking industry significantly. Customers now expect fast, convenient, and digital banking services through mobile apps, internet banking, and automated systems. While technology improves efficiency, it also creates pressure on banks to constantly upgrade their systems.

Many traditional banks struggle to keep up with technological advancements due to the high cost of digital transformation. Outdated banking systems may become slow, inefficient, and vulnerable to security risks. Banks must continuously invest in modern software, digital infrastructure, and employee training to remain competitive.

The rise of financial technology companies, commonly known as fintech companies, has increased competition in the industry. Companies such as PayPal and Stripe provide fast and convenient financial services that challenge traditional banks.

Economic Instability

Economic instability is another major challenge facing banks worldwide. Inflation, recession, unemployment, currency fluctuations, and rising interest rates can negatively affect banking operations.

During economic downturns, many individuals and businesses struggle to repay loans, leading to an increase in bad debts and loan defaults. This affects the profitability and financial stability of banks. Economic crises can also reduce customer savings and investments.

For example, the Global Financial Crisis caused severe damage to banks around the world. Many financial institutions suffered huge losses due to risky lending practices and poor financial management.

Banks must therefore develop strong risk management strategies to survive periods of economic uncertainty.

Strict Government Regulations

Banks operate under strict rules and regulations imposed by governments and financial authorities. These regulations are designed to protect customers, prevent fraud, and maintain financial stability. However, complying with these regulations can be expensive and time-consuming.

Banks are required to meet capital requirements, maintain accurate financial records, monitor suspicious transactions, and follow anti-money laundering laws. Failure to comply with regulations may result in heavy fines, legal penalties, and reputational damage.

Regulatory changes can also affect banking operations. Banks must frequently update their policies and systems to meet new legal requirements, which increases operational costs.

Competition from Fintech Companies

The emergence of fintech companies has changed the financial industry dramatically. Fintech firms provide innovative services such as mobile payments, online lending, cryptocurrency trading, and digital wallets.

Unlike traditional banks, many fintech companies operate with lower costs and faster digital services. They attract younger customers who prefer convenient online transactions over visiting physical bank branches.

This competition forces traditional banks to improve their technology, customer service, and digital banking platforms. Banks that fail to adapt risk losing customers and market share.

In Africa, mobile banking platforms such as M-Pesa have transformed the financial sector by providing easy payment solutions to millions of users.

Loan Default and Credit Risk

Banks make profits mainly by lending money to individuals, businesses, and governments. However, one major risk is the inability of borrowers to repay loans. This is known as credit risk or loan default.

When borrowers fail to repay loans, banks lose money and may face financial difficulties. Economic hardship, unemployment, poor business performance, and inflation often increase loan defaults.

Banks must carefully evaluate customers before granting loans. They use credit checks, collateral requirements, and financial analysis to reduce lending risks. Despite these measures, loan defaults remain a major challenge in the banking industry.

Loss of Customer Trust

Trust is one of the most important foundations of banking. Customers expect banks to protect their money and personal information. However, financial scandals, fraud cases, hidden charges, and poor customer service can reduce public confidence in banks.

When customers lose trust, they may withdraw their funds or switch to other financial institutions. Negative publicity spreads quickly through social media, making reputational damage even more serious.

Banks must therefore maintain transparency, honesty, and good customer relationships to preserve public trust.

Read: What is Mortgages: Types, Interest Rates, and How to Repay”

High Operational Costs

Running a bank involves huge operational expenses. Banks spend large amounts of money on employee salaries, branch maintenance, technology systems, cybersecurity, electricity, compliance, and customer support services.

In many countries, maintaining physical branches has become expensive due to rising operational costs. As a result, some banks reduce branch networks and encourage customers to use digital banking services instead.

High operating costs can reduce profitability, especially for smaller banks that struggle to compete with larger financial institutions.

Money Laundering and Financial Crimes

Banks face constant threats from money laundering, terrorism financing, and other illegal financial activities. Criminal organizations sometimes attempt to use banks to hide illegally obtained money.

Financial crimes damage the reputation of banks and may result in severe legal consequences. Governments and international organizations require banks to monitor transactions carefully and report suspicious activities.

Banks now use advanced software and compliance systems to detect unusual financial transactions. However, financial criminals continue to develop new methods to bypass banking controls.

Changing Customer Expectations

Modern customers expect quick, simple, and personalized banking services. People want to access their accounts anytime and anywhere using smartphones and computers. Long waiting times, poor customer service, and outdated systems can frustrate customers.

Younger generations especially prefer digital experiences and fast online support. Banks that fail to meet customer expectations may lose clients to competitors.

To remain relevant, banks must improve customer experience, provide reliable digital platforms, and offer personalized financial products.

Globalization and International Risks

Globalization has connected financial systems around the world. While this creates opportunities for international banking and investment, it also increases risks.

Economic problems in one country can quickly affect banks in other countries. Exchange rate fluctuations, international conflicts, trade restrictions, and global pandemics can disrupt banking activities worldwide.

For example, the COVID-19 pandemic affected banking operations globally by reducing economic activities and increasing financial uncertainty.

Banks involved in international trade and finance must carefully manage global risks and maintain strong financial reserves.

Environmental and Climate Risks

Climate change is becoming an important concern for the banking industry. Natural disasters such as floods, droughts, hurricanes, and wildfires can damage businesses, properties, and agricultural activities financed by banks.

Banks may suffer losses if borrowers affected by environmental disasters cannot repay loans. Investors and governments now expect banks to support environmentally responsible projects and reduce investments in harmful industries.

As a result, many banks are adopting sustainable banking practices and supporting green finance initiatives.

Shortage of Skilled Workforce

Modern banking requires highly skilled workers with knowledge of technology, cybersecurity, finance, and risk management. Finding and retaining qualified employees has become challenging for many banks.

Rapid technological changes mean that employees must continuously learn new skills. Banks invest heavily in staff training and development to improve productivity and service delivery.

Competition for skilled professionals from fintech companies and global organizations has also increased workforce challenges in the banking sector.

Political and Policy Uncertainty

Political instability and sudden government policies can affect banking operations significantly. Changes in taxation, monetary policies, interest rates, and foreign exchange regulations can create uncertainty in the banking environment.

In some countries, political crises may lead to inflation, currency depreciation, or reduced investor confidence. Banks operating in unstable environments often face increased financial risks.

Strong economic and political stability are therefore important for a healthy banking system.

Read: What is Fiscal Policy: Objectives and Types

The Future of Banking

The future of banking is strongly connected to technology and innovation. Artificial intelligence, blockchain technology, and digital currencies are changing the financial industry rapidly.

Many banks now use artificial intelligence to improve customer service, detect fraud, and analyze financial data. Online banking continues to grow as more customers prefer digital transactions over physical banking.

Cryptocurrencies such as Bitcoin have also introduced new ideas about decentralized finance. Although cryptocurrencies remain controversial in some countries, they have influenced discussions about the future of money and banking.

Cashless economies are becoming more common, especially in developed countries. Mobile payments and contactless transactions are reducing dependence on physical cash.

However, trust, security, and regulation will remain essential in the future of banking. Regardless of technological changes, banks will continue to play a central role in economic development and financial stability.

Conclusion

The history and origin of banking show how human societies developed systems to manage wealth, support trade, and promote economic growth. From ancient temples in Mesopotamia to modern digital banking platforms, banking has evolved continuously to meet the changing needs of people and businesses.

Ancient civilizations introduced basic banking practices such as deposits and loans, while Greek and Roman societies expanded financial services. During the Middle Ages, goldsmiths and merchants contributed to the growth of banking, and Italian bankers later established many modern banking principles.

The Industrial Revolution and technological advancements transformed banking into a global industry that supports governments, businesses, and individuals worldwide. Today, banking remains one of the most powerful institutions in the global economy.

As technology continues to reshape financial services, the banking industry will keep evolving. Yet the main purpose of banking remains the same as it was thousands of years ago: providing safe, reliable, and efficient ways for people to manage money and support economic activities.

Contact: Kokobest04@gmail.com

- HELOC vs Home Equity Loan: What Is the Difference? - June 27, 2026

- Wells Fargo Credit Card: Benefits, Features, and How to Choose the Best One - June 18, 2026

- What is Letters of Credit: Definition, Types, and Usage - June 16, 2026