Last Updated on June 16, 2026 by admin

In today’s interconnected global economy, businesses frequently engage in international trade, buying and selling goods across borders. While international trade creates opportunities for growth and expansion, it also introduces significant risks.

Sellers may worry about receiving payment after shipping goods, while buyers may be concerned about paying for products that do not arrive or fail to meet agreed standards. To address these concerns, financial institutions provide various trade finance instruments, one of the most important being the Letter of Credit (LC).

A Letter of Credit serves as a financial guarantee that helps establish trust between buyers and sellers who may have never met or conducted business before. By involving a bank as an intermediary, both parties gain confidence that their obligations will be fulfilled according to the terms of the agreement. As a result, Letters of Credit have become a cornerstone of international trade and commerce.

This article explores the concept of Letters of Credit, their definition, types, benefits, challenges, and practical applications in modern business transactions.

Read: Fixed vs. Variable Mortgage Rates: What Canadians Need to Know

What is a Letter of Credit?

A Letter of Credit is a formal document issued by a bank on behalf of a buyer, guaranteeing payment to a seller provided that the seller meets specific conditions outlined in the credit agreement. These conditions usually require the seller to present certain documents proving that the goods have been shipped or services have been delivered as agreed.

In simple terms, a Letter of Credit acts as a promise from the buyer’s bank that the seller will receive payment if all contractual requirements are met. This arrangement reduces the risk for both parties and promotes smooth business transactions.

For example, imagine a company in Canada purchasing machinery from a manufacturer in Germany. The German seller may hesitate to ship expensive equipment without assurance of payment. Similarly, the Canadian buyer may not want to pay before receiving the machinery. A Letter of Credit bridges this trust gap by ensuring that payment will be made once the seller provides the required shipping and commercial documents.

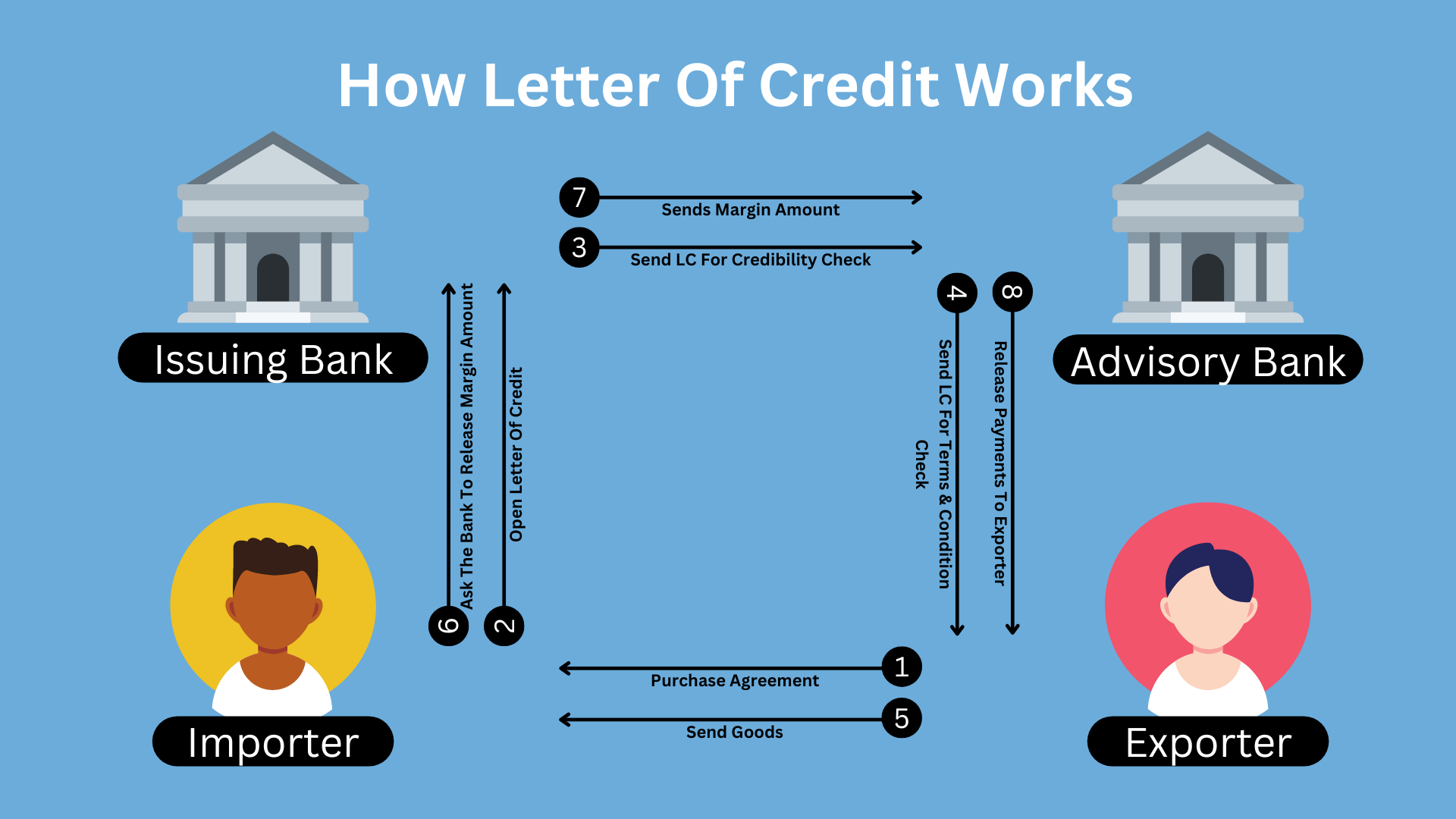

How a Letter of Credit Works

The process of using a Letter of Credit generally follows several key steps:

- The buyer and seller agree on the terms of a sales contract.

- The buyer requests a Letter of Credit from their bank.

- The issuing bank creates the Letter of Credit and sends it to the seller’s bank.

- The seller reviews the terms and ships the goods.

- The seller submits the required documents to their bank.

- The bank verifies that the documents comply with the Letter of Credit terms.

- Payment is made to the seller.

- The buyer receives the documents needed to claim the goods.

This process ensures that payment is tied to documentary evidence rather than personal trust alone.

Key Parties Involved in a Letter of Credit

Several parties participate in a Letter of Credit transaction:

Applicant

The applicant is the buyer who requests the Letter of Credit from their bank.

Beneficiary

The beneficiary is the seller who will receive payment once the terms of the Letter of Credit are satisfied.

Issuing Bank

The issuing bank creates the Letter of Credit and guarantees payment on behalf of the buyer.

Advising Bank

The advising bank receives the Letter of Credit from the issuing bank and notifies the seller about its issuance.

Confirming Bank

In some cases, a second bank adds its guarantee to the Letter of Credit. This bank is known as the confirming bank.

Negotiating Bank

The negotiating bank reviews documents and may provide payment to the seller before receiving reimbursement from the issuing bank.

Each participant plays an important role in ensuring that the transaction proceeds smoothly and securely.

How Much Do Letters of Credit Cost?

The cost of a Letter of Credit is usually calculated as a percentage of the total transaction amount. Most banks charge between 0.5% and 2% of the Letter of Credit value per year, although rates can vary depending on the bank and the customer’s creditworthiness.

For example, if a company requests a Letter of Credit worth $100,000, the issuing bank may charge between $500 and $2,000 annually. In some cases, banks charge fees quarterly rather than annually.

Read: Canada Mortgage and Housing Corporation (CMHC):Its Role, Functions, and Impact

Types of Letters of Credit

Letters of Credit come in different forms depending on the needs of the buyer and seller.

1. Revocable Letter of Credit

A revocable Letter of Credit can be modified or canceled by the issuing bank without prior notice to the beneficiary.

Because it offers limited protection to sellers, this type is rarely used in international trade today.

2. Irrevocable Letter of Credit

An irrevocable Letter of Credit cannot be changed or canceled without the consent of all parties involved.

This is the most commonly used type because it provides stronger security and certainty.

3. Confirmed Letter of Credit

A confirmed Letter of Credit includes an additional guarantee from another bank.

This arrangement is useful when the seller is uncertain about the financial stability of the issuing bank or the political environment of the buyer’s country.

4. Unconfirmed Letter of Credit

An unconfirmed Letter of Credit relies solely on the guarantee of the issuing bank.

While less expensive, it may expose the seller to additional risks.

5. Sight Letter of Credit

Under a sight Letter of Credit, payment is made immediately after the required documents are presented and verified.

This option provides quick access to funds for the seller.

6. Usance or Deferred Payment Letter of Credit

Payment under a usance Letter of Credit is made at a future date, such as 30, 60, or 90 days after document presentation.

This arrangement gives buyers additional time to generate revenue from the goods before making payment.

7. Transferable Letter of Credit

A transferable Letter of Credit allows the beneficiary to transfer some or all of the credit to another party.

This type is often used by intermediaries and trading companies.

8. Standby Letter of Credit

A standby Letter of Credit functions as a backup payment guarantee.

Payment is made only if the buyer fails to fulfill contractual obligations.

Standby Letters of Credit are commonly used in construction projects, service agreements, and long-term contracts.

9. Revolving Letter of Credit

A revolving Letter of Credit automatically renews after use, making it suitable for businesses engaged in regular transactions with the same trading partner.

This reduces administrative work and improves efficiency.

Benefits of Letters of Credit

Letters of Credit provide numerous advantages to buyers, sellers, and banks.

Reduced Risk

One of the primary benefits is risk reduction. Sellers gain confidence that payment is guaranteed by a reputable financial institution, while buyers know that payment will only occur when agreed conditions are met.

Enhanced Trust

International trade often involves parties located in different countries with different legal systems and business practices.

A Letter of Credit creates trust where personal relationships may not exist.

Improved Cash Flow

Sellers can access financing based on the security of a Letter of Credit.

This helps improve cash flow and supports business operations.

Facilitates International Trade

Letters of Credit make it easier for businesses to enter new markets and establish relationships with foreign partners.

Without such financial instruments, many international transactions would be considered too risky.

Legal Protection

The detailed terms and documentation requirements provide a clear framework for resolving disputes and ensuring compliance.

Read: Different between FHA Loans vs. Conventional Loans

How to Apply for a Letter of Credit

The first step in applying for a Letter of Credit is to agree on the terms of the transaction with the seller. Both parties should clearly define the amount, shipment details, required documents, and payment conditions.

Next, the buyer approaches their bank and submits an application for the Letter of Credit. The bank may require supporting documents such as a purchase agreement, invoice, company registration documents, and financial statements. The bank will also assess the buyer’s creditworthiness before approving the request.

Once approved, the bank issues the Letter of Credit and sends it to the seller’s bank. The seller can then ship the goods according to the agreed terms. After shipment, the seller submits the required documents to their bank for verification.

If all conditions of the Letter of Credit are met, the issuing bank releases payment to the seller. This process helps ensure secure and reliable transactions for both buyers and sellers, especially in international business.

Challenges and Limitations of Letters of Credit

Despite their advantages, Letters of Credit are not without challenges.

Complexity

Preparing and reviewing the required documents can be complicated and time-consuming.

Even small errors may lead to payment delays or rejection of documents.

Cost

Banks charge fees for issuing, advising, confirming, and processing Letters of Credit.

These costs can be significant, especially for smaller businesses.

Strict Compliance Requirements

Banks operate under the principle of strict compliance.

This means documents must exactly match the terms specified in the Letter of Credit.

Minor discrepancies may result in payment complications.

Processing Time

The verification and approval process may take several days or weeks, depending on the complexity of the transaction.

Dependence on Documentation

Banks deal with documents rather than actual goods.

As a result, a compliant set of documents does not necessarily guarantee that the goods themselves meet quality expectations.

Common Documents Required in a Letter of Credit Transaction

Several documents are commonly required to satisfy Letter of Credit conditions:

Commercial Invoice

This document details the goods sold, quantity, price, and payment terms.

Bill of Lading

The bill of lading serves as proof that goods have been shipped.

Packing List

This document outlines the contents of each shipment package.

Certificate of Origin

The certificate of origin identifies the country where the goods were manufactured.

Insurance Certificate

This document confirms that the shipment is insured against loss or damage.

Inspection Certificate

An inspection certificate verifies that the goods meet specified standards or quality requirements.

The exact documentation required varies depending on the terms of the Letter of Credit.

Read: What Is a Debt Consolidation Loan and How Does It Work?

Practical Example of a Letter of Credit

Consider a textile importer in Canada purchasing fabric from a supplier in India.

The supplier is concerned about receiving payment, while the importer wants assurance that the fabric will be shipped as agreed.

The importer requests an irrevocable Letter of Credit from their bank.

The bank issues the credit and sends it to the supplier’s bank.

After receiving confirmation, the supplier manufactures and ships the fabric.

The supplier then submits the required shipping documents to their bank.

Once the documents are verified and found compliant, payment is released according to the terms of the Letter of Credit.

Both parties complete the transaction with reduced financial risk.

The Role of Letters of Credit in Modern4 Trade

Letters of Credit continue to play a crucial role in global commerce despite advances in digital payment technologies.

International trade involves various uncertainties, including political instability, currency fluctuations, legal differences, and transportation risks. Letters of Credit help mitigate these concerns by providing a structured and secure payment mechanism.

Many industries rely heavily on Letters of Credit, including manufacturing, agriculture, energy, construction, and retail. Companies engaged in large-value transactions particularly benefit from the security and confidence these instruments provide.

Furthermore, technological innovations are transforming the traditional Letter of Credit process. Electronic documentation, blockchain technology, and digital trade platforms are making transactions faster, more transparent, and more efficient.

As global trade continues to expand, Letters of Credit remain an essential tool for facilitating business relationships and reducing commercial risk.

Conclusion

Letters of Credit are among the most important financial instruments used in domestic and international trade. They provide a reliable framework that protects both buyers and sellers by ensuring that payment obligations are met according to agreed terms.

By involving banks as trusted intermediaries, Letters of Credit reduce uncertainty, build confidence, and support business growth across borders. Various types of Letters of Credit exist to address different commercial needs, from immediate payment arrangements to long-term contractual guarantees.

Although they can be complex and involve costs, their benefits often outweigh the challenges, particularly in high-value or international transactions. For businesses seeking to expand globally, understanding how Letters of Credit work is essential for managing risk and conducting successful trade operations.

In an increasingly interconnected world, Letters of Credit continue to serve as a vital bridge between trust and commerce, enabling companies to engage in trade with greater security, confidence, and efficiency.

Contact: Kokobest04@gmail.com