Last Updated on May 12, 2026 by admin

Whether someone wants to buy a house, apply for a car loan, secure funding for a business, or even obtain a credit card, lenders often assess the borrower’s financial reliability before approving the request. Two major tools commonly used in this process are credit ratings and credit scores. Although these terms are often used interchangeably, they are not the same thing. They serve different purposes, apply to different entities, and are calculated in different ways.

Understanding the distinction between credit ratings and credit scores is essential because both influence financial opportunities, borrowing costs, and overall financial reputation. While a credit score usually relates to individuals and their personal borrowing behavior, a credit rating is more commonly associated with corporations, governments, and large institutions. Both systems are designed to measure creditworthiness, but they operate on different scales and are used by different audiences.

This essay explains the meaning of credit ratings and credit scores, highlights their differences, explores how they are calculated, and discusses their importance in modern finance.

Read: Definition of Credit Unions and How They Compare to Banks

What is Credit Scores

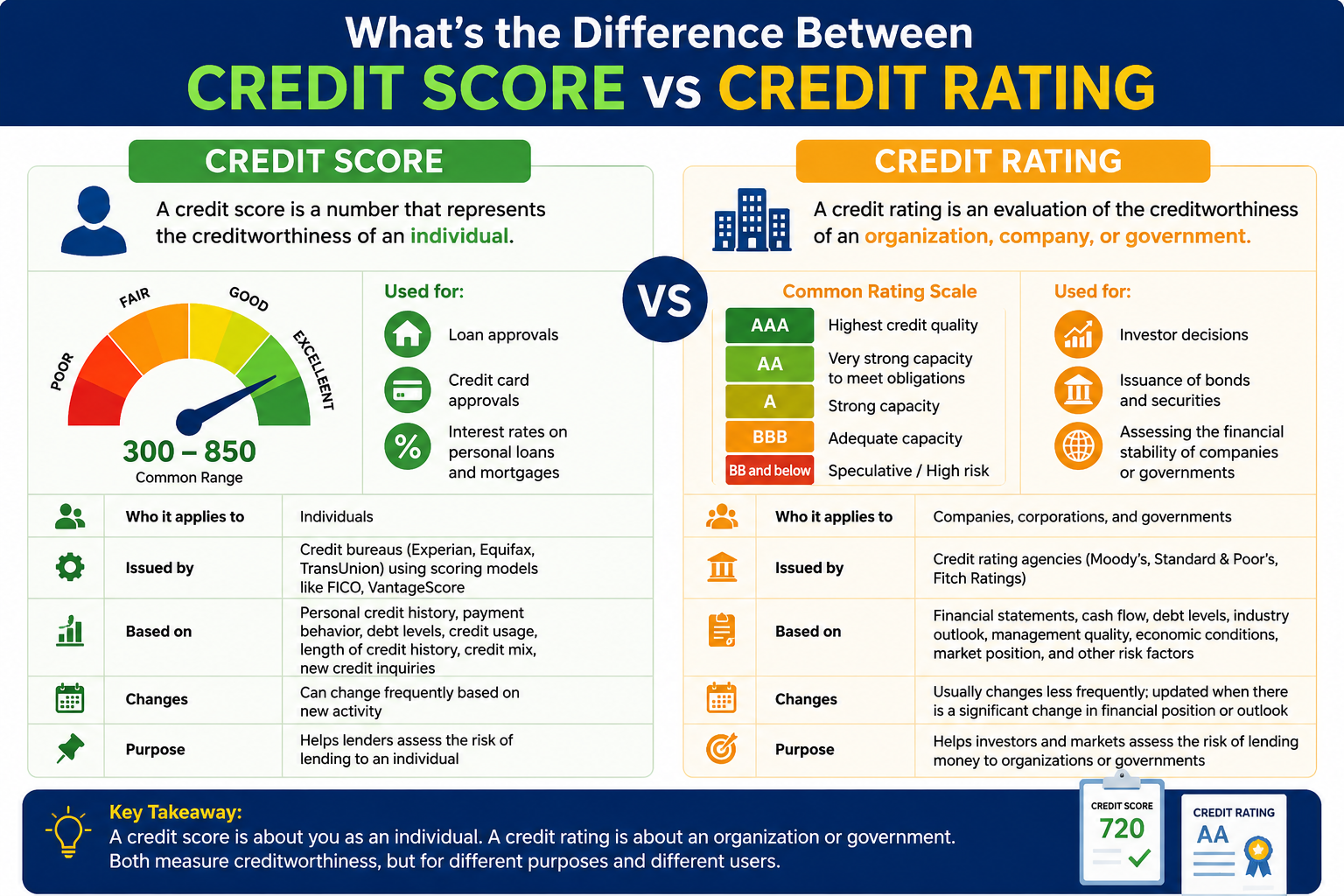

A credit score is a numerical representation of an individual’s creditworthiness. In simple terms, it shows how likely a person is to repay borrowed money responsibly. Financial institutions such as banks, mortgage lenders, and credit card companies use credit scores to evaluate the risk involved in lending money to a person.

Credit scores are usually calculated using information from an individual’s credit history. This information includes borrowing habits, repayment behavior, debt levels, and the length of time the person has used credit facilities. The most widely known credit scoring models globally are the FICO Score and VantageScore.

Credit scores generally range from 300 to 850. A higher score indicates stronger financial reliability, while a lower score suggests higher lending risk. Although exact classifications may vary slightly among financial institutions, the following categories are commonly used:

- 300–579: Poor credit

- 580–669: Fair credit

- 670–739: Good credit

- 740–799: Very good credit

- 800–850: Excellent credit

A person with an excellent credit score is more likely to qualify for loans with lower interest rates because lenders consider them financially trustworthy. On the other hand, individuals with poor credit scores may struggle to secure loans or may face higher borrowing costs.

Several factors influence credit scores. Payment history is one of the most important elements because lenders want evidence that borrowers repay debts on time. Credit utilization, which measures how much of the available credit a person is using, also plays a major role. Other factors include the length of credit history, types of credit accounts, and recent credit inquiries.

For example, if an individual consistently pays credit card bills on time, keeps debt levels low, and avoids excessive borrowing, their credit score is likely to improve over time. However, missed payments, loan defaults, or bankruptcy can significantly reduce a credit score.

Read: How to Get Loan Without BVN Stress in Nigeria (For Salary Earners)

What is Credit Ratings

Unlike credit scores, credit ratings are evaluations of the creditworthiness of organizations, businesses, or governments rather than individuals. A credit rating reflects the ability of an entity to repay its financial obligations, particularly debts such as bonds or loans.

Credit ratings are issued by specialized agencies known as credit rating agencies. The most prominent agencies globally are Moody’s Corporation, Standard & Poor’s, and Fitch Ratings. These agencies analyze financial statements, economic conditions, debt levels, and management quality before assigning ratings.

Credit ratings are usually expressed using letter grades rather than numerical scores. For example:

- AAA or Aaa: Highest credit quality

- AA: Very strong capacity to meet obligations

- A: Strong but somewhat vulnerable to economic conditions

- BBB: Adequate capacity to repay debt

- BB and below: Speculative or high-risk investments

A company or government with a high credit rating is considered financially stable and less likely to default on debt repayments. As a result, investors are more willing to lend money to such entities at lower interest rates. Conversely, organizations with poor credit ratings are viewed as risky borrowers and often pay higher interest rates to attract investors.

For instance, if a government receives a downgrade in its credit rating, international investors may lose confidence in its economy. This can increase borrowing costs and negatively affect economic growth. Similarly, corporations with weak credit ratings may find it difficult to raise capital for expansion or operations.

Credit ratings are especially important in financial markets because investors rely on them when making investment decisions. They provide a quick assessment of the level of risk associated with purchasing corporate or government bonds.

Factors that influence your credit score

The five main factors that influence your credit score are:

- Payment history (35%) — Do you pay on time? This is the biggest chunk.

- Credit utilisation (30%) — How much of your available credit are you actually using?

- Length of credit history (15%) — How long have your accounts been open?

- Credit mix (10%) — Do you have a variety of credit types (loans, cards, mortgages)?

- New credit (10%) — Have you recently applied for new lines of credit?

A credit score is used by banks, landlords, phone companies, and even some employers to make decisions about you. Applying for a mortgage? They’ll check it. Renting a flat? Almost certainly. Getting a new phone contract? Yep, that too.

Differences Between Credit Ratings and Credit Scores

Although both credit ratings and credit scores assess creditworthiness, there are several important differences between them.

1. Evaluation

The most obvious difference lies in who or what is being evaluated. Credit scores apply mainly to individuals, while credit ratings are generally assigned to corporations, governments, and financial institutions.

For example, a worker applying for a personal loan will likely be assessed using a credit score. In contrast, a multinational company issuing bonds to investors will receive a credit rating.

2. Format of Measurement

Credit scores are represented numerically, usually within a fixed range such as 300 to 850. Credit ratings, however, use letter-based grades such as AAA, AA, BBB, or BB.

This distinction reflects the different purposes of the two systems. Numerical scores are more suitable for evaluating individual consumers, while letter grades provide a broad assessment of institutional financial strength.

3. Issuing Bodies

Credit scores are generated by credit bureaus and scoring models using automated systems and financial data. Common credit bureaus include Experian, Equifax, and TransUnion.

Credit ratings, on the other hand, are issued by credit rating agencies after detailed financial analysis and professional evaluation.

4. Purpose

Credit scores primarily help lenders decide whether to approve loans or credit applications for individuals. They are heavily used in personal finance decisions such as mortgages, student loans, and credit card approvals.

Credit ratings are mainly used by investors and financial markets to evaluate the risk associated with lending money to organizations or governments.

5. Factors Considered

Credit scores focus largely on personal borrowing behavior, including payment history, debt usage, and credit account management.

Credit ratings consider broader financial and economic factors such as profitability, cash flow, political stability, market conditions, management efficiency, and economic outlook.

6. Frequency of Changes

Credit scores can change frequently because they are updated whenever new financial information is reported. Missing a single payment may reduce a person’s score quickly.

Credit ratings usually change less frequently because they involve long-term assessments of institutional financial health. However, major economic or financial events can trigger sudden upgrades or downgrades.

Importance of Credit Scores

Credit scores have become increasingly important in everyday financial life. Many lenders use them as a quick and reliable tool for assessing financial responsibility. A strong credit score offers several benefits.

First, individuals with high credit scores often enjoy easier access to loans and credit facilities. Financial institutions see them as low-risk borrowers, making approval more likely.

Second, good credit scores can lead to lower interest rates. Over time, this can save borrowers substantial amounts of money, especially on long-term loans such as mortgages.

Third, credit scores may influence non-lending decisions. In some countries, landlords, insurance companies, and even employers review credit histories before making decisions.

Maintaining a healthy credit score therefore requires financial discipline. Paying bills on time, avoiding unnecessary debt, and monitoring credit reports regularly are important practices for building strong creditworthiness.

Importance of Credit Ratings

Credit ratings are equally important in the broader financial system. They help investors assess risk before committing funds to governments or corporations.

For businesses, a strong credit rating can reduce borrowing costs and improve access to capital markets. Companies with high ratings are often viewed as stable and trustworthy, making them more attractive to investors.

Governments also depend heavily on credit ratings. Sovereign credit ratings affect a country’s ability to borrow internationally and influence foreign investment inflows. A downgrade in sovereign credit rating may weaken investor confidence and increase economic pressure.

Credit ratings also contribute to transparency in financial markets. By providing independent evaluations, rating agencies help investors make informed decisions about risk and return.

However, credit rating agencies have sometimes faced criticism, especially after the 2008 global financial crisis. Some analysts argued that certain risky financial products received overly favorable ratings, contributing to financial instability. Despite such criticisms, credit ratings remain an important component of global finance.

Similarities Between Credit Ratings and Credit Scores

Despite their differences, credit ratings and credit scores share some similarities.

Both are measures of creditworthiness and financial reliability. They aim to predict the likelihood that a borrower will repay debt obligations responsibly.

Both systems influence borrowing costs. Higher scores or ratings generally lead to lower interest rates, while lower evaluations increase borrowing expenses.

Additionally, both rely heavily on financial history and current financial conditions. Whether assessing an individual or a corporation, past financial behavior is often considered an indicator of future reliability.

Finally, both systems significantly affect financial opportunities. A poor credit score can limit personal borrowing options, just as a poor credit rating can restrict a company’s ability to raise capital.

Read: What is Mortgages: Types, Interest Rates, and How to Repay”

How to improve Your Credit Score: Practical Steps

Since credit scores are the thing most individuals can directly influence, it’s worth knowing how to move that number upward.

Pay on time, every time. This is the single most impactful thing you can do. Even one missed payment can cause a noticeable dip. Set up automatic payments if you’re prone to forgetting.

Keep your utilisation low. Aim to use no more than 30% of your available credit at any given time. If your limit is £5,000, try to keep your balance under £1,500. If you can get it below 10%, even better.

Don’t close old accounts. The age of your credit history matters. That old card you never use? Keep it open (as long as it has no annual fee). It’s quietly helping your score just by existing.

Limit hard enquiries. Every time you apply for new credit, it triggers a “hard enquiry” on your report. A few are fine, but a flurry of applications in a short period signals desperation to lenders.

Check your report for errors. Mistakes happen. An account wrongly marked as delinquent, or a debt that isn’t yours, can drag your score down unfairly. In many countries, you’re entitled to a free credit report annually — use it.

Read: What is Fiscal Policy: Objectives and Types

Conclusion

Credit ratings and credit scores are essential tools in modern financial systems, but they serve different purposes and apply to different entities. A credit score is mainly designed for individuals and reflects personal borrowing behavior using a numerical scale. In contrast, a credit rating evaluates the financial strength of corporations, governments, and institutions using letter-based grades.

While credit scores help lenders assess individual borrowers, credit ratings guide investors in evaluating the risks associated with organizations and sovereign entities. Both systems influence access to credit, borrowing costs, and financial reputation.

Understanding the distinction between credit ratings and credit scores is important for anyone seeking to navigate the financial world effectively. Individuals who maintain strong credit scores can enjoy better financial opportunities, while organizations with strong credit ratings are better positioned to attract investment and secure funding. Ultimately, both concepts highlight the importance of financial responsibility, transparency, and trust in economic relationships.

Contact: Kokobest04@gmail.com

- Wells Fargo Credit Card: Benefits, Features, and How to Choose the Best One - June 18, 2026

- What is Letters of Credit: Definition, Types, and Usage - June 16, 2026

- Fixed vs. Variable Mortgage Rates: What Canadians Need to Know - June 9, 2026